Financial Fitness: 7 Habits for Achieving Long-Term Prosperity.

Achieving long-term prosperity isn’t about quick fixes or overnight success. It’s about cultivating habits that build financial fitness over time. Just as physical fitness requires consistent exercise and healthy eating, financial fitness demands disciplined saving, smart investing, and mindful spending. Here are seven essential habits to develop for long-term financial health and prosperity.

1. Set Clear Financial Goals

Setting clear financial goals is the foundation of financial fitness. Without a clear destination, it’s impossible to chart a course. Begin by identifying your short-term and long-term financial goals. Short-term goals might include paying off credit card debt, creating an emergency fund, or saving for a vacation. Long-term goals could involve buying a home, funding your children’s education, or planning for retirement.

Action Steps:

- SMART Goals: Ensure your goals are Specific, Measurable, Achievable, Relevant, and Time-bound.

- Write Them Down: Document your goals and review them regularly to stay motivated and on track.

- Break It Down: Divide larger goals into smaller, manageable milestones to make them less daunting.

2. Create and Stick to a Budget

A budget is a critical tool for managing your finances. It helps you track your income and expenses, ensuring that you live within your means and allocate resources towards your goals.

Action Steps:

- Track Your Spending: Use apps or spreadsheets to monitor your daily expenses.

- Categorize Expenses: Divide your spending into essential (needs) and non-essential (wants) categories.

- Adjust Accordingly: Regularly review and adjust your budget to reflect changes in income or expenses.

Proven Expert Tips for Building a Solid Financial Portfolio

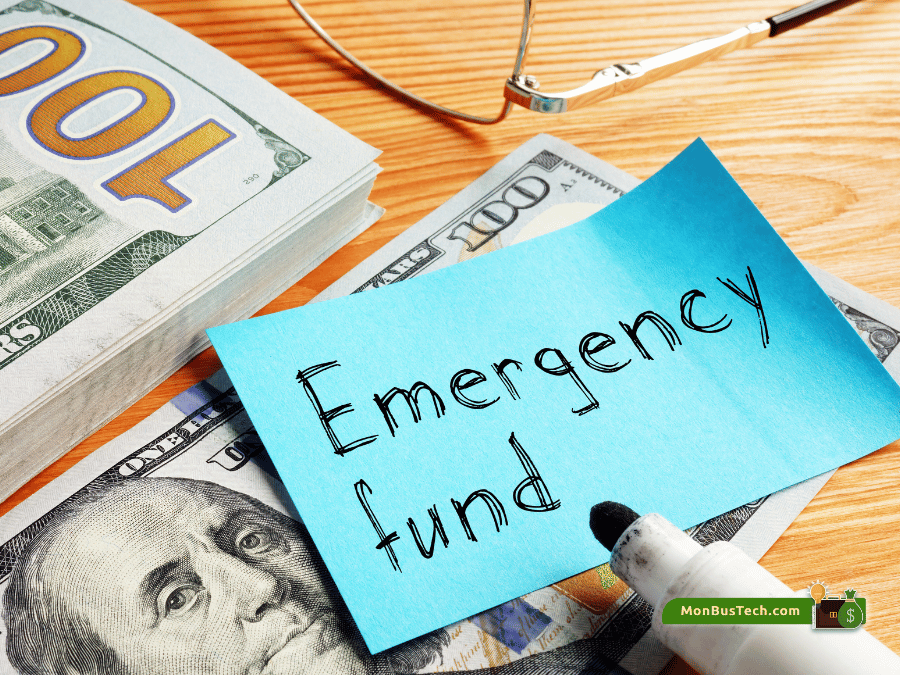

3. Build an Emergency Fund

An emergency fund acts as a financial safety net, protecting you from unexpected expenses like medical emergencies, car repairs, or job loss. Without an emergency fund, you might be forced to rely on credit cards or loans, leading to debt.

Action Steps:

- Start Small: Aim to save at least $1,000 initially, then work towards accumulating three to six months’ worth of living expenses.

- Automate Savings: Set up automatic transfers to your emergency fund to ensure consistent contributions.

- Keep It Accessible: Store your emergency fund in a high-yield savings account where it can grow yet remain easily accessible.

4. Eliminate High-Interest Debt

High-interest debt, such as credit card balances, can severely hamper your financial health. Paying off this debt should be a priority, as it will free up more money for savings and investments.

Action Steps:

- List Your Debts: Write down all your debts, including interest rates and minimum payments.

- Debt Snowball Method: Focus on paying off the smallest debt first while making minimum payments on the others. Once the smallest is paid off, move to the next smallest, and so on.

- Debt Avalanche Method: Alternatively, pay off the debt with the highest interest rate first to minimize interest payments over time.

5. Invest for the Future

Investing is key to growing your wealth over the long term. While saving is important, investing allows your money to work for you, generating returns that outpace inflation and build your financial future.

Action Steps:

- Educate Yourself: Learn the basics of investing, including different asset classes (stocks, bonds, mutual funds, ETFs).

- Diversify: Spread your investments across various assets to minimize risk.

- Contribute Regularly: Consistently invest a portion of your income, taking advantage of compound interest.

6. Plan for Retirement

Retirement planning is crucial for long-term financial health. Starting early can significantly impact the amount you accumulate, thanks to the power of compound interest.

Action Steps:

- Utilize Employer Plans: Contribute to employer-sponsored retirement plans like 401(k)s, especially if your employer offers matching contributions.

- Open an IRA: If you don’t have access to a retirement plan through work, consider opening an Individual Retirement Account (IRA).

- Increase Contributions: Gradually increase your retirement contributions over time to maximize your savings.

Profitable Side Hustles: 20 Ideas for Earning Extra Income

7. Continually Educate Yourself

Financial literacy is an ongoing journey. Staying informed about personal finance, investment strategies, and economic trends is essential for making informed decisions.

Action Steps:

- Read Books and Articles: Regularly read books, blogs, and articles on personal finance and investing.

- Attend Workshops and Seminars: Participate in financial workshops and seminars to enhance your knowledge and network with like-minded individuals.

- Follow Experts: Follow reputable financial experts and economists on social media and subscribe to their newsletters.

Conclusion

Achieving long-term prosperity requires more than just making money; it involves managing, saving, and investing wisely. By setting clear goals, creating and adhering to a budget, building an emergency fund, eliminating high-interest debt, investing for the future, planning for retirement, and continually educating yourself, you can build a solid foundation for financial fitness. These habits will not only help you achieve financial stability but also allow you to enjoy the fruits of your labor, providing peace of mind and a prosperous future.

Incorporate these habits into your daily life, and you’ll be well on your way to achieving long-term financial success. Remember, financial fitness is a journey, not a destination. Stay committed, stay disciplined, and watch your prosperity grow.